· deep dive · 16 min read

Amazon Leo | 231 Satellites, 90 Days, and a Deadline That Will Not Move

As of late April 2026, Amazon has 231 production satellites in orbit after eleven launches. The FCC license requires 1,618 by July 30. The math, the rockets, and what happens when the calendar runs out on a mega-constellation.

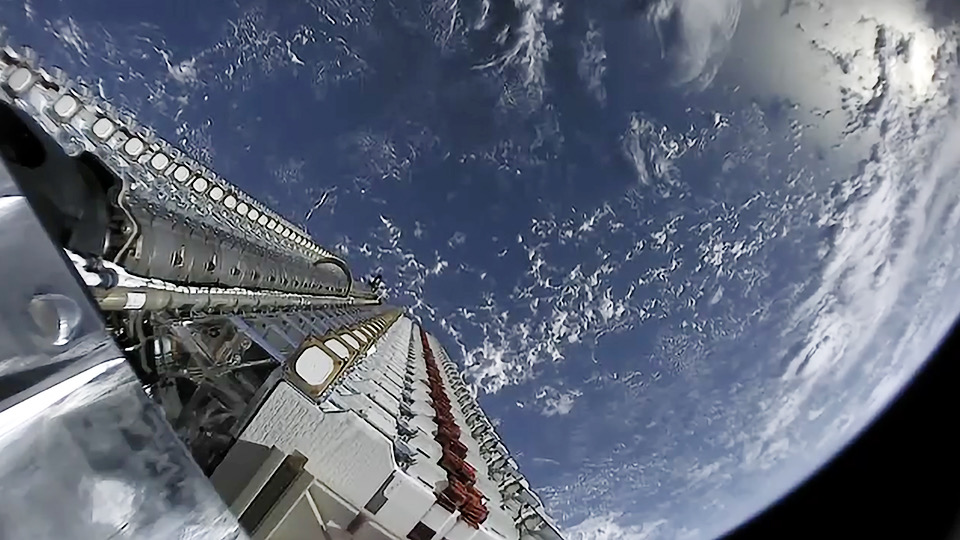

On April 27, 2026, an Atlas V lifted off from Cape Canaveral’s SLC-41 carrying 29 satellites with a name nobody outside Amazon was using two years ago. The mission was LA-06. The payload was the latest tranche of what is now called Amazon Leo - the constellation formerly known as Project Kuiper, rebranded in 2025 in a move that traded the cold poetry of an outer-solar-system ice belt for the unambiguous business clarity of a three-letter orbital regime. The new name is shorter. It also tells you what Amazon needs you to remember: this is a low Earth orbit broadband network, and Amazon is the company building it.

The rebrand was a tell. Project Kuiper had been an aspirational name for a paper constellation - announced in 2019, with two prototype satellites flown in October 2023, and then, for eighteen months, mostly silence. Amazon Leo is what the program is called now that hardware is actually flying in volume. It is a name that wants to compete in the same conversation as Starlink, OneWeb, and a coming generation of state-backed Chinese constellations. It is also a name that arrives at a moment of acute regulatory pressure, because the FCC license that lets Amazon build this thing in the first place comes with a deadline that is now, by any honest measure, mathematically out of reach.

As of the LA-06 launch, Amazon Leo has 231 production satellites in orbit, plus the two original KuiperSat prototypes that flew on a ULA Atlas V in October 2023 and have since been deorbited. Eleven launches have put those satellites up - one prototype mission and ten production missions, spread across three different rocket families and beginning in earnest with LA-01 in April 2025. That is roughly one production launch per month for a year. It is a remarkable industrial cadence by historical standards. It is also a long way from where Amazon needs to be.

The FCC license, granted in July 2020, requires Amazon to have 1,618 satellites in orbit - half of the authorized 3,236-satellite constellation - by July 30, 2026. As of this writing, Amazon is at 231. Three months remain. The arithmetic is unforgiving.

What’s Up There Now

The 231 satellites are not yet a usable broadband network. They are the beginning of one. Amazon has not announced commercial service availability, has not published subscriber numbers, and has not set retail pricing for its three terminal classes. What it has done is establish that the satellite production line works, that the launch cadence is real, and that the architecture - three altitude shells, optical inter-satellite links, Ka-band user service, K-band gateways - can be deployed at the rate Amazon’s industrial partners need to deliver.

The satellites that flew on LA-06 are essentially identical to the ones that flew on LA-05 three weeks earlier, and on LA-04 before that. Each Atlas V mission carries 27 to 29 satellites depending on configuration. Each one drops them into one of the three operational shells at altitudes between 590 and 630 kilometers. Each one then waits for the satellites to raise themselves to their final operational orbits, deploy their solar arrays, run through commissioning, and join the small but growing operational network.

The two KuiperSat prototypes from 2023 - KuiperSat-1 and KuiperSat-2 - are no longer part of that count. They were technology demonstrators rather than production hardware, and after validating the platform’s basic systems they were deorbited as planned. They served their purpose. The 231 production satellites currently aloft are what Amazon Leo actually is.

1,387

Satellites short of the FCC milestone

Amazon needs 1,618 satellites in orbit by July 30, 2026, to meet its license condition. With 231 currently flying and three months remaining, the gap is the story.

The July 30 Problem

The FCC’s 50-percent-by-2026 deadline is not new. It was written into Amazon’s authorization in July 2020 as a standard milestone condition - the same kind of “use it or lose it” provision the FCC routinely attaches to non-geostationary satellite system licenses. The intent is simple: an authorization is a promise to build, not a parking spot for spectrum. If Amazon cannot demonstrate progress, the FCC reserves the right to revisit the license, reduce the authorized satellite count, or in extreme cases reclaim the spectrum entirely.

Amazon’s response has been to petition for an extension. The company filed with the FCC in early 2026 asking for additional time, citing the unprecedented technical challenges of standing up an entirely new space-based business at industrial scale - what its filings characterize as a “first-of-kind” undertaking. The filing language is careful. It does not concede that the deadline is unmeetable; it argues that the deadline as originally written did not anticipate the realities of satellite supply chains, launch availability, and the engineering schedules of a fully new bus design.

The risk is real but not existential. The FCC has historically granted partial relief on milestone deadlines for non-geostationary systems when the petitioner can show good-faith progress. SpaceX received accommodation on its V-band schedule. OneWeb’s deadlines were renegotiated through Chapter 11. The likely outcome here is some form of restructured milestone rather than license cancellation - but the terms of any extension will shape what Amazon Leo looks like in 2027 and beyond.

What the FCC will actually do is unknowable in advance, but the precedent is instructive. The Commission has shown a willingness to renegotiate milestone schedules when an operator is clearly building - launching, deploying, generating commerce - rather than warehousing spectrum. Amazon, with eleven launches and 231 satellites and a documented industrial program, is not in the warehousing category. It is in the “building hard, behind schedule” category, which is where most large mega-constellation operators have spent at least part of their licensed lifetimes.

The harder question is what an extension would cost. Amazon’s authorization is bounded in two dimensions: time and satellite count. The most likely outcome of an FCC negotiation is a stretched timeline tied to a phased-deployment schedule, possibly with milestone-by-milestone certifications. A less likely outcome is a reduction in the authorized satellite count - the FCC trading additional time for a smaller authorized constellation. A worst-case outcome, which observers regard as unlikely, is partial spectrum forfeiture. Each of these has different downstream consequences for the architecture Amazon has been building.

How Amazon Got Here

The launch cadence story is the most encouraging part of Amazon’s situation, even though it is also the part that explains why the deadline is in trouble. Production launches did not begin until April 2025 - five years after the FCC authorization. The two prototypes flew in late 2023, and then nothing flew for sixteen months while Amazon finalized its production satellite design, set up its Kirkland production facility, and waited for ULA to make Atlas V capacity available.

KuiperSat-1 and KuiperSat-2

Two prototype satellites launched on a ULA Atlas V from SLC-41 to validate platform systems. Both have since been deorbited.

LA-01 (KA-01)

First production launch. ULA Atlas V from SLC-41. 27 satellites delivered to operational shell.

LA-02 (KA-02)

Second production batch on Atlas V. Cadence begins establishing.

LA-03

Third production mission. Cape Canaveral SLC-41.

LA-04

Fourth production batch. Continued Atlas V execution.

First Falcon 9 Kuiper mission

SpaceX Falcon 9 carries Amazon Leo satellites from the Eastern Range under a previously announced multi-launch contract.

Ariane 6 contribution

First Arianespace Ariane 6 mission carrying Amazon Leo satellites. Diversification of launch base.

Continued Atlas V cadence

Additional production missions through Q1 2026 maintain monthly delivery rhythm.

LA-05

29 satellites on Atlas V from SLC-41. Production count crosses 200.

LA-06

29 satellites on Atlas V from SLC-41. Production count reaches 231. Most recent mission.

LA-07 (planned)

Next scheduled Atlas V mission. Continued cadence ahead of FCC deadline negotiations.

The dates above include some approximations for the middle-2025 missions because Amazon’s public disclosure of individual launch identifiers has been inconsistent - the company sometimes uses LA-NN designators, sometimes KA-NN, sometimes neither. What is not approximated is the headline number: 231 production satellites in orbit after eleven total flights, with the most recent two launches landing within twenty-three days of each other.

That April 2026 cadence - LA-05 on the 4th and LA-06 on the 27th - is the highest tempo Amazon has achieved. It is also approximately the cadence the company would need to sustain, on multiple rocket families simultaneously, to bring the constellation anywhere near the originally licensed deployment schedule. Sustaining it is hard. Atlas V will not be available much longer. Falcon 9 manifests are crowded. Ariane 6 is still ramping. New Glenn has flown but not yet at the cadence Amazon needs.

The Three Shells

Amazon Leo’s orbital architecture is one of its most distinctive features and one of the things that most clearly differentiates it from Starlink. Where Starlink’s first shell sat in a single 550 km band and its later shells extended that approach with relatively modest variation, Amazon Leo is built around three deliberately separated altitude shells at 590 km, 610 km, and 630 km, each with its own characteristic inclination - approximately 30 degrees, 42 degrees, and 52 degrees respectively.

The architectural logic is coverage tailoring. Each inclination band serves a specific latitude range with optimal pass geometry. The 30-degree shell concentrates capacity at low latitudes. The 42-degree shell extends coverage into the mid-latitudes where most population lives. The 52-degree shell reaches into the higher latitudes that matter for North American and European service. Together, the three shells deliver a coverage profile that Amazon’s planners argue is more efficient for global broadband than a single inclined shell tilted to compromise across all latitudes.

| Shell | Altitude | Inclination | Role |

|---|---|---|---|

| Shell 1 | 590 km | ~30° | Low-latitude high-density coverage |

| Shell 2 | 610 km | ~42° | Mid-latitude population centers |

| Shell 3 | 630 km | ~52° | Higher-latitude reach (US, Europe) |

| Total | — | — | 3,236 satellites across 98 orbital planes |

The trade-off is complexity. A three-shell architecture means three distinct deployment campaigns, three sets of plane-and-spacing requirements, three different launch trajectory profiles, and three different Atlas V or Falcon 9 mission designs. Starlink’s relative architectural uniformity made its early launches interchangeable - any Falcon 9 could carry any Starlink batch to roughly any operational slot. Amazon Leo cannot quite do that. Each launch targets a specific shell and plane, which constrains how quickly the constellation can be reshaped if one launch slips or one rocket family becomes unavailable.

The user-link and feeder-link architecture is more conventional. Ka-band serves user terminals; K-band serves the gateway and AWS Ground Station feeder links. Optical inter-satellite links (OISL) connect satellites within and between planes, allowing traffic to be routed through the constellation rather than always returning to a ground station near the user. This is the same architectural pattern Starlink adopted with its laser-link generation, and it is now the de facto standard for any mega-constellation that wants to provide service in regions without dense gateway infrastructure.

What Amazon Leo Is Actually For

If Amazon Leo were trying to win the residential consumer broadband race, it would already have lost. Starlink has roughly seven thousand satellites in orbit and has crossed five million subscribers globally. Its terminal-and-service product is mature, its installer ecosystem is real, and its brand recognition among rural-broadband consumers is now effectively unrivaled. The runway for a second consumer-LEO entrant is narrow at best.

Amazon’s positioning, articulated through its filings and public communications, is different. The headline pillars are AWS integration, enterprise and government sales, and fixed broadband for institutional customers - airlines, maritime, oil and gas, utilities, telecom backhaul. Amazon Leo is not designed first as a consumer ISP. It is designed first as an extension of AWS - a satellite layer that connects AWS Ground Station, AWS Direct Connect, and AWS regions in a way that makes the entire AWS edge story tighter for customers who need to compute, store, or move data from places terrestrial fiber does not reach.

| Operator | Satellites in orbit | Subscribers | Annual revenue (est.) | Service status |

|---|---|---|---|---|

| Starlink (SpaceX) | ~7,000+ | 5M+ | $4B+ (2024 extrapolated) | Mature global service |

| Amazon Leo | 231 | 0 (pre-launch) | $0 | Pre-commercial |

| OneWeb (Eutelsat Group) | ~650 | Enterprise/wholesale | Embedded in Eutelsat consolidated | Operational, B2B |

| Telesat Lightspeed | 0 | 0 | $0 | In construction |

The terminal lineup reflects this positioning. The residential terminal is targeted at roughly $400 - lower than Starlink’s standard kit on launch, which is a deliberate signal that Amazon understands consumer price points even if consumers are not the primary customer. The mobile or compact terminal is positioned around $200, designed for transportable and small-form-factor use cases. The enterprise terminal sits at roughly $1,500 and is built for the institutional customers Amazon actually wants to win.

The Project Kuiper for U.S. Government division - the federal-facing arm of the program, kept under the older Kuiper branding for continuity with existing relationships - is the other strategic axis. AWS already has a deep federal customer base through GovCloud and a variety of intelligence community contracts. A satellite layer that integrates natively with that infrastructure is a credible differentiation play in a market where Starshield is currently the dominant offering. Whether that integration can be delivered fast enough to matter is the question the FCC deadline indirectly answers.

The Atlas V Bridge

The story of how Amazon Leo got its first 231 satellites into orbit is, more than anything else, a story about Atlas V. The same vehicle that has been carrying U.S. national security and NASA payloads for two decades is now in the final phase of its operational life, and Amazon is its largest single end-of-life customer. ULA originally allocated nine Atlas V missions to the Kuiper program, with options for additional flights as the manifest evolved. Six of those missions have flown, including LA-06 on April 27. The remaining Atlas V Kuiper missions are scheduled to deplete the allocation by approximately LA-09.

After that, Atlas V is done. The vehicle’s component supply chain - particularly the Russian RD-180 first-stage engines that Atlas V was originally built around - has been wound down for years, and ULA has been carefully managing its remaining inventory to fulfill its existing manifest. Amazon Leo gets its last Atlas V flights and then has to find capacity elsewhere.

The deployment of a first-of-kind satellite constellation at this scale, on a fully new bus design and across multiple launch families, presents technical and supply-chain challenges that warrant a milestone schedule reflecting the realities of building such a system.

The Atlas V bridge has been essential. Without it, Amazon would not have a launch cadence at all - it would have been waiting for Vulcan Centaur to ramp up, for Falcon 9 manifest slots, for Ariane 6’s first commercial flights, and for New Glenn to demonstrate commercial reliability. Atlas V’s reliability and SLC-41 launch infrastructure gave Amazon a platform from which to begin actual deployment in 2025 rather than late 2026. That head start is the only reason 231 satellites are in orbit today.

It is also the reason the post-Atlas V transition matters so much. Vulcan Centaur is contracted for the bulk of Amazon’s remaining ULA flights and is now operational, but it is still ramping its annual cadence. Falcon 9 has carried Amazon payloads under contracts that predate the rebrand, and is the most reliable cadence vehicle in the world, but Amazon’s manifest competes with SpaceX’s own Starlink missions. Ariane 6 has begun contributing - one Amazon Leo flight at minimum - but Arianespace’s cadence has its own development arc. New Glenn, Blue Origin’s heavy-lift vehicle, is the long-term piece that Amazon’s parent ownership argues should eventually carry a meaningful share of the constellation, but its commercial operational tempo is still being established.

What Comes Next

The next ninety days are the most consequential of the program. LA-07 is currently scheduled for May 22, 2026 - a third Atlas V mission in two months. Beyond that, the publicly disclosed manifest tightens up but does not stop. Amazon has signaled an intent to maintain monthly cadence on Atlas V through the remainder of its allocation, transitioning into Vulcan Centaur and Falcon 9 capacity as Atlas V flights are exhausted, with Ariane 6 and New Glenn picking up additional capacity through 2027.

Commercial service launch has been targeted for late 2026 or early 2027. Amazon has not committed to a specific date publicly. The dependency is twofold: enough satellites in orbit to provide meaningful coverage, and enough ground infrastructure to support real customer traffic. Amazon’s AWS Ground Station service provides the backbone of the latter; the former is the gating item. With 231 satellites today, Amazon could plausibly stand up beta service in selected geographic markets by year-end 2026, particularly along the lower-latitude belt where the 590 km / 30-degree shell concentrates capacity.

The competitive context outside Amazon’s own program does not stand still. Starlink continues to add satellites at a cadence that Amazon will not match in 2026 - SpaceX is launching multiple Starlink missions per week, with the v3 generation now flying and direct-to-cell capacity expanding. AST SpaceMobile’s BlueBird constellation is addressing the direct-to-cell market that Amazon Leo is not currently designed for. ViaSat-3 F3 is launching on Falcon Heavy on May 2, refilling geostationary capacity in its third orbital slot. The HTS market is being reshaped almost monthly. And on May 3, Hughes is bringing additional Ka-band capacity online under terms that further reshape the enterprise broadband landscape Amazon is trying to enter.

Amazon Leo is not late to a static market. It is late to a market that is reshaping itself faster than the constellation can be deployed.

The Bigger Picture

The honest framing of where Amazon Leo stands in late April 2026 is this: the program is real, the satellites are flying, the production line works, and the launch cadence has been demonstrated to be roughly one mission every three to four weeks at peak tempo. The program is also significantly behind the schedule that the FCC license originally contemplated, and the next ninety days will determine what kind of regulatory accommodation Amazon receives.

The deeper lesson is what mega-constellations actually demand from the companies that build them. SpaceX’s headstart on Starlink looks, in retrospect, less like a clever competitive move and more like a baseline cost of entry. Five thousand satellites is not the goal line for a mega-constellation; it is the price of admission. Reaching that price requires not just capital - Amazon has $10 billion of disclosed program commitment, which is approximately what Starlink had consumed by the time it crossed the same satellite count - but also production capacity, launch capacity, regulatory runway, and the institutional patience to absorb three or four years of negative cash flow before service revenue begins to matter.

Amazon has all of those things. What it does not have, on April 27, 2026, is the satellite count its own license requires. That is a problem the FCC will help solve, in some form, because the alternative - cancelling or fundamentally restructuring an authorization to a flagship American technology company that is actively launching - is not in the Commission’s interest. But the terms of that solution will tell us something real about how the United States now thinks about mega-constellation regulation.

The 231 satellites are real. The eleven launches are real. The July 30 deadline is also real. The space between them is where the next quarter of Amazon Leo’s history will be written - in FCC filings, in additional Atlas V flights, in Vulcan and Falcon and Ariane manifests, and eventually in the first paying enterprise and government customers signing contracts for a service that has been promised for seven years and is now, finally, close enough to credibly sell.

For KeepTrack users, the 231 satellites are already in the catalog. They will be joined, on current schedule, by 29 more on May 22 when LA-07 flies. Each subsequent batch will appear as it reaches operational orbit. The constellation that does not yet exist as a service is already, in a strict orbital sense, the third-largest commercial broadband network in space. The question of when - and on what terms - it becomes the second-largest is the one the next ninety days will begin to answer.

References(10)

- Project Kuiper Updates and Mission Reports - Amazon

- Kuiper Systems LLC: Authorization for a Non-Geostationary Satellite System (FCC IBFS File No. SAT-LOA-20190704-00057)

- Kuiper Systems Milestone Schedule Modification Petition - FCC IBFS, 2026 (Amazon)

- Amazon Leo (Project Kuiper) - Wikipedia

- ULA Atlas V Kuiper Mission Press Materials - United Launch Alliance

- Atlas V Launches 29 Amazon Kuiper Satellites on LA-06 Mission - Spaceflight Now, April 27, 2026

- Atlas V Lofts More Amazon Internet Satellites on LA-06 - Space.com, April 27, 2026

- Project Kuiper - eoPortal Directory, European Space Agency

- NASASpaceflight Coverage of Project Kuiper / Amazon Leo Launch Manifest

- Amazon.com 2024 Annual Report and Investor Disclosures (Project Kuiper / Amazon Leo capital commitments)

Theodore Kruczek